Fair Finance Asia Launches New Report Highlighting Consumer Empowerment Case Studies in Cambodia, Indonesia, Pakistan, and Thailand

Fair Finance Asia (2026, July), Empowering Consumers as Partners in Sustainability: Case Studies on Financial Regulation and Implementation.

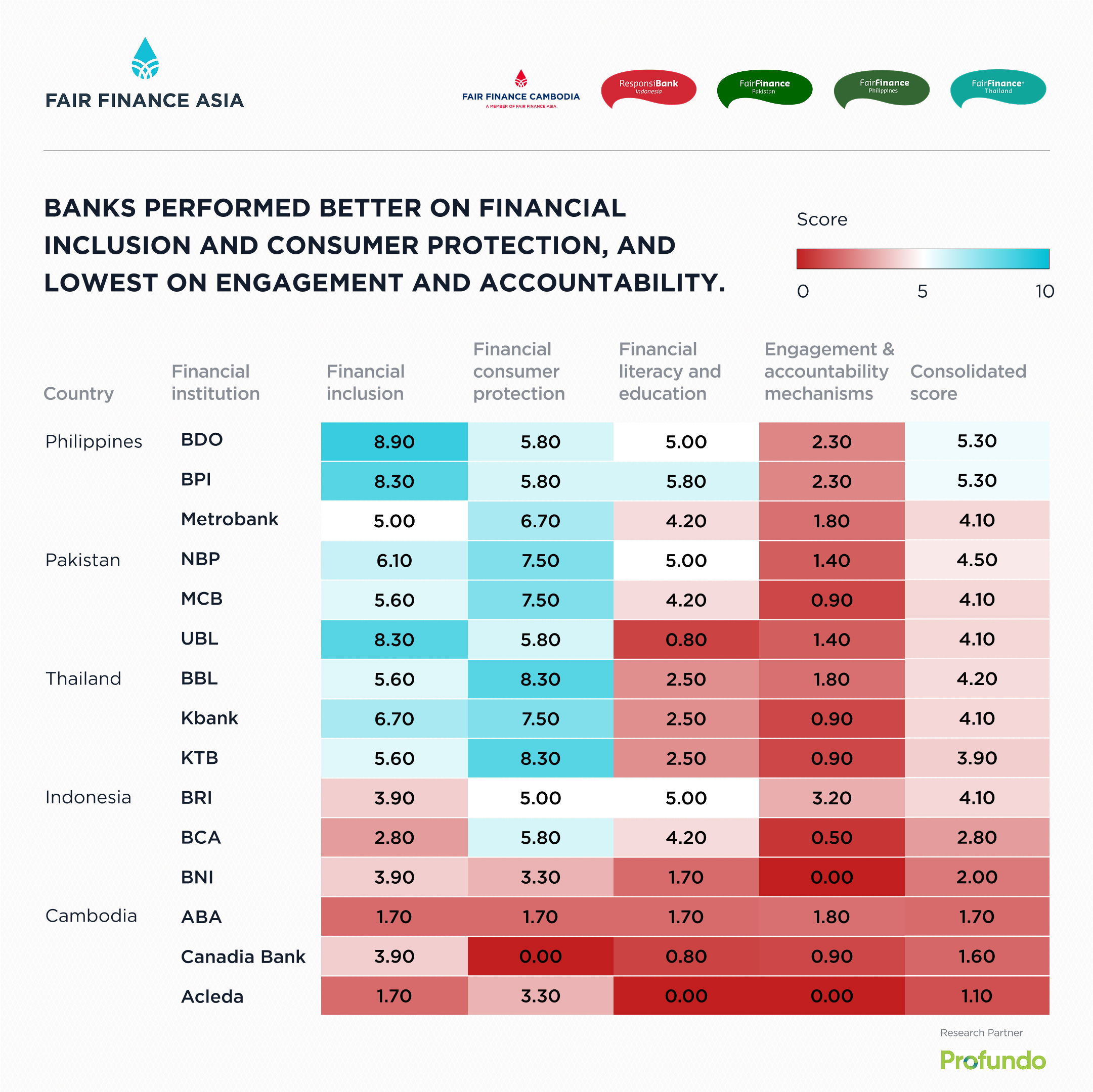

Fair Finance Asia (FFA) and research partner, Profundo, have launched a new report, Empowering Consumers as Partners in Sustainability: Case Studies on Financial Regulation and Implementation, on the experiences of banking consumers across Asia and examining how financial regulations are implemented in practice. Building on FFA’s 2024 consumer empowerment scorecard, the report features four case studies from Cambodia, Indonesia, Pakistan, and Thailand, covering financial inclusion, consumer protection, financial literacy and education, and consumer engagement and accountability mechanisms. It was developed in collaboration with Fair Finance Cambodia (FFC), ResponsiBank Indonesia, Fair Finance Pakistan (FFP), and Fair Finance Thailand (FFT).

Consumer Cybersecurity Risk in Thailand

The Thailand case study examines the growing prevalence of cybersecurity fraud, highlighting how perpetrators exploit online platforms, mobile applications, and identity theft to deceive victims and steal funds. While Thai banks achieved the highest average consumer protection score among the countries assessed, the report finds that elderly and digitally excluded customers remain exposed to social engineering tactics. Critical gaps include limited financial literacy programs for retail customers, inconsistent coverage of third-party banking agents, optional security notifications, and the lack of interim compensatory relief for fraud victims.

Recommendations for financial institutions:

- All security alerts should be free and enabled automatically.

- Complaint mechanisms should be monitored transparently.

- Training should be provided to consumers on cybersecurity threats and sound financial management.

Recommendations for the Bank of Thailand (BoT):

- Regulate human-facing scam tactics.

- Mandate consumer education for vulnerable groups.

Empowering Women Entrepreneurs in Pakistan

The Pakistan case study examines the financial inclusion of women entrepreneurs and women-led micro-, small, and medium-sized enterprises (MSMEs). While the three Pakistani banks assessed scored above the overall average for financial inclusion and offered products targeting unbanked and underbanked populations, awareness gaps remain the immediate barrier preventing women entrepreneurs from accessing financial products and services. Although the regulatory landscape has significantly improved, implementation and enforcement gaps continue to weaken the policy framework.

Recommendations for financial institutions:

- Conduct transparent and proactive public outreach through relevant and accessible channels.

- Tailor communication for customers with low digital literacy.

- Provide structured community outreach programs.

Recommendations for the State Bank of Pakistan (SBP)

- Adopt an impact-driven approach to target setting and monitoring.

- Introduce intermediate milestones and a response framework.

- Expand the monitoring and evaluation framework.

Consumer Engagement and Accountability Mechanisms in Indonesia

The Indonesia case study examines consumer and community complaints about the environmental and social impacts of banks’ lending activities. Indonesian banks received the lowest scores on consumer engagement and accountability mechanisms, revealing a lack of systems and channels for consumers to engage with banks on sustainability issues. The report also identifies significant transparency gaps, with consumers unable to assess the real-world impact of their deposits and investments, and highlights obstacles faced by consumers and civil society organizations in holding banks accountable for environmental and social due diligence.

Recommendations for Indonesian banks:

- Establish non-judicial environmental, social, and governance (ESG) grievance mechanisms.

- Respond to stakeholder concerns.

- Enhance portfolio transparency.

- Proactive sustainability engagement.

- Strengthen ESG due diligence.

Recommendations for regulators, especially Otoritas Jasa Keuangan (OJK)/Financial Services Authority:

- Broaden the scope of mandatory disclosure.

- Mandate third-party assurance of sustainability reporting.

- Mandate client consent to disclosure in high-risk sector lending.

- Advocate for and help design mandatory human rights and environmental due diligence (HREDD) law applicable to the financial sector.

- Enforce strict penalties for misleading sustainability claims.

- Support judicial and regulatory training on sustainable finance.

Overindebtedness in Cambodia

The Cambodia case study examines overindebtedness and complaint handling processes for consumers. While financial consumer protection emerged as the highest-scoring theme overall, Cambodian banks received the lowest average score. The report identifies persistent gaps between the regulatory framework and consumers’ lived experiences, including inadequate debt burden assessments, inconsistent complaint handling, abusive debt collection practices, and the continued use of vulnerable collateral, indicating that existing safeguards are not yet consistently applied across the sector.

Recommendations for Cambodian banks:

- Comply with the Code of Conduct for Banking and Financial Institutions (BFIs).

- Conduct a detailed, systematic, and documented assessment of borrowers’ ability to repay their loans.

- Restrict collateral practices to avoid cumulative impacts of overindebtedness.

- Develop responsible debt collection guidelines.

- Extend ethical business standards to third parties.

- Strengthen complaints handling.

- Enhance the transparency and accountability of complaints resolution.

Recommendations for the National Bank of Cambodia (NBC):

- Mandate annual public audits on consumer protection.

- Standardize repayment capacity assessments.

- Cap recovery fees.

- Impose sanctions for unethical practices.

- Support the FCPC.

- Ban high-risk collateral via directive.

Access the full case studies and recommendations here.

More information:

- Read FFA’s 2025 scored benchmarking 15 Asian banks on consumer empowerment here.